|

|

| Tsang |

Accused of being overly committed to laissez-faire policy making in the past, Hong Kong is grabbing the bull by its horns with the proposed tax incentives for corporate treasury centres. A few percentage points savings on treasury-related income alone are unlikely to sway corporates to centralize their Asian treasury operations in the territory. Together with the opening of China’s capital account, though, they offer an appealing package.

Hong Kong’s financial secretary John Tsang unveiled a package of tax incentives in his February budget speech, including a 50% profits tax reduction on “specified treasury activities” and fewer restrictions on interest deductions for corporate treasury centres. The proposal will be introduced in the 2015-2016 session and, if passed, amend the Inland Revenue Ordinance.

Currently, income arising from corporate treasury activities (from interest on loans to affiliates, for example) is subject to 16.5% profits tax, while interest expense deductions are subject to complicated restrictions. Generally they are only permitted if the interest is subject to Hong Kong profits tax, a distinction that Singapore, for instance, does not make.

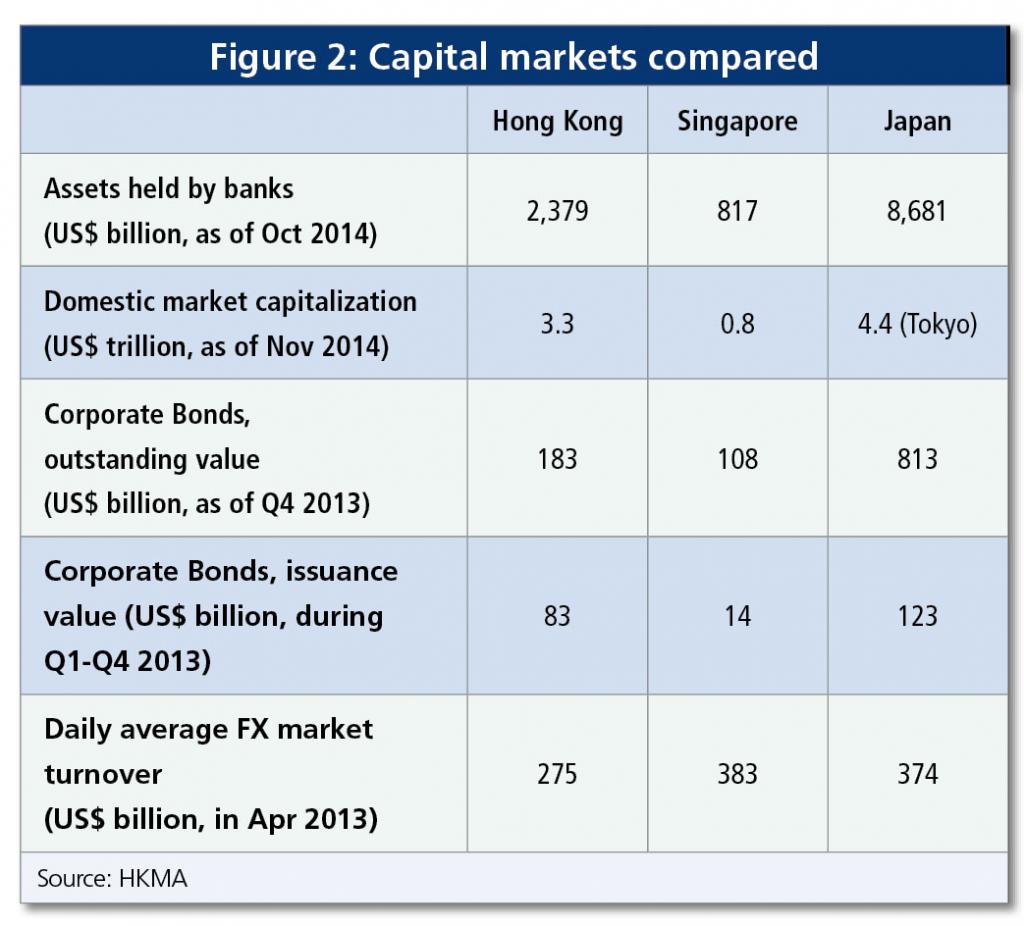

Under the planned revision, income from treasury activities will be subject to an effective tax rate of 8.25%, lower than what companies in Singapore are charged for these types of activities (See table 1).

The proposed incentives will “remove the key tax impediments for corporate treasury centres operating in Hong Kong”, says EY financial services tax partner James Badenach, thereby strengthening the territory’s position vis-à-vis other jurisdictions keen on capitalizing on efforts by corporates to centralize their treasury operations in the region.

PwC believes that as a result of the tax cuts, more than 4,000 treasury-related jobs could be created in Hong Kong if they attract corporate treasury centres equivalent to just 25% of the number already established in Singapore.

“The existing tax law on interest expense deduction is definitely not favourable for setting up a treasury centre in Hong Kong, and as a result, Hong Kong-based businesses looked elsewhere to establish their internal treasury functions,” says Jeremy Choi, tax partner at PwC.

“The industry had been calling for changes for some time and the proposals are very good news not only for Hong Kong companies but also for multinationals, which will now be given another option to consider.”

A Hong Kong-based treasury executive of a large multinational echoes the view: “Some of the regional treasuries here will be pleased about the incentives and Hong Kong stands to become more attractive.”

However, he cautions that “the pie is pretty well divided already so the question is who will decide to move to Hong Kong because of the tax measures”.

Indeed, relocating a company’s regional treasury centre (RTC) will involve enormous management adjustments, staff movements and logistical considerations that disrupt operations even if only in the short term, hence, a lower tax rate alone may not be enough to convince corporates to transfer their RTCs to Hong Kong.

Those whose regional treasury operations are already located in Hong Kong will, of course, welcome the proposed incentives.

|

|

One CFO of a French multinational whose Asian RTC is domiciled in Hong Kong says the new rules will make a difference in group funding considerations. The company structures intercompany loans so as to centralize interest margins in France, where interest expenses are deductible and can be consolidated with other entities.

“Now, we will consider case by case when they come, whether putting Hong Kong in the loop makes sense,” the CFO adds.

Other treasurers told The Asset they prefer to wait for the actual legislation due later this year before evaluating the impact on their current operations.

One of the central areas of concern is what exactly will define “specified treasury activities” eligible for the concessionary profits tax rate of 8.25%. Depending on the scope of tasks entrusted to the treasury entity, different sources of income may arise.

They can be grouped in three broad categories: cash and liquidity management services (such as payments and collections on behalf of entities throughout the group), corporate finance activities (including intercompany loans) and financial market risk management activities (including hedging of foreign exchange and interest rate exposures at the regional level).

Hence, in addition to interest income from loans to affiliate companies, centralized corporate treasury entities may receive service fee income and see gains (or losses) on positions they have taken as a result of their hedging activities.

Ultimately, says EY’s Badenach, the activities eligible for preferential tax treatment will be those that Hong Kong is seeking to attract. “We would assume that service fees and interest margin would be included, but other types of income such as trading gains and losses on managing foreign currency exchange, interest rate and commodity risks may or may not be included,” he notes.

When sought for details of the tax incentives, a spokesperson for the Hong Kong Monetary Authority (HKMA) says the government will launch an industry consultation to further define qualifying corporate treasury centres, treasury services and transactions as well as related mechanisms.

|

|

| Choi |

Do taxes matter?

Taxation of treasury activities is just one of many considerations corporates weigh when deciding where to centralize their treasuries. Last year, the Financial Services and Treasury Bureau (FSTB) and the HKMA tasked EY to identify the main factors that multinationals and Chinese enterprises consider in the selection of location. The firm found that the regulatory environment including FX controls, costs and availability of staff, political stability and access to capital markets were equally important.

A look at Singapore, where the likes of Cargill, Daimler, ExxonMobil, IBM, Nestle, Shell, Midea and China Oilfield Services have chosen to centralize their Asia treasury operations, further underscores that tax rates on treasury income play a more peripheral role for many corporates than expected. According to Badenach, many of the RTCs in Singapore do not in fact avail themselves of the city state’s finance and treasury centre incentive package.

Clearly, with its well-developed banking system and efficient capital markets, common law legal system and its (lower) tax regime, Hong Kong ticks many of the other boxes identified as important by corporates. So does Singapore, which has attracted a larger share of corporate treasury centres.

EY’s survey of corporates in the region did find, however, that jurisdictions like China and Malaysia have the upper hand in attracting lower value-added functions, such as payment processing and operational-type treasury activities.

Malaysia, in particular, is trying to move up the chain, with some success. An incentive package is available for corporates conducting regional or global treasury management activities for their group of related companies from Malaysia.

The incentives include a 70% tax exemption on treasury-related income (which translates into an effective tax rate of 7.5%), exemptions on withholding taxes and concessions on income tax applicable to expatriate staff sent to Malaysia. Eight treasury management centres (TMCs) with combined investments of 186.9 million ringgit (US$51 million) had been approved at the end of 2014, four more than a year earlier.

According to the Malaysian Investment Development Authority, the TMCs are expected to create 130 jobs in the country. Most of them were established by Malaysian corporates such as Axiata, and one was set up by a Hong Kong corporate.

|

|

| Badenach |

China reform boosts HK

Hong Kong is aware that headline tax concessions alone are unlikely to matter much to corporates in their decision making.

The HKMA spokesperson also notes the “impressive progress” in negotiating double taxation agreements with other jurisdictions, up from just five in 2009 to 32 at the end of 2014.

But success in communicating this progress to corporates appears to be less impressive. “From our interviews, it is clear that there is a perception gap between how MNCs perceive Hong Kong’s DTA network and the reality,” says EY’s Badenach.

“Hong Kong’s DTA network is wider and of better quality (for corporate treasury centres) than is generally perceived, and the gap between Hong Kong and Singapore is narrower than what a straight numerical comparison (32 versus 76, respectively) indicates and in particular with Hong Kong’s treaties providing for a lower rate than many of Singapore’s treaties and the coverage of Hong Kong and China’s key trading partners.”

The application of bilateral DTAs is considered the most important tax factor in location selection by corporates approached for comment, Badenach asserts.

More important than the progress authorities in Hong Kong have made in this regard, however, are likely to be developments outside of their control. In November, the People’s Bank of China announced a landmark reform that plays in Hong Kong’s favour. Under the new scheme, eligible mainland Chinese and foreign-invested corporates in China are allowed to set up renminbi-denominated cross-border cash pooling structures (see December issue of The Asset) from anywhere in the country. For many MNCs, this means the integration of their regional and China treasury operations is within reach for the first time.

With renminbi deposits in the territory exceeding 1.1 trillion renminbi, Hong Kong offers these multinationals the largest offshore pool of the Chinese currency anywhere in the world – more than 4x the size of Singapore’s. For corporates seeking to centralize risk exposure of their Chinese entities, Hong Kong promises an efficient foreign exchange market for CNH instruments and other currencies. According to the Bank for International Settlements, Hong Kong is the fifth largest FX activity centre with average daily turnover of FX transactions at US$275 billion.

This will also appeal to mainland Chinese enterprises with growing international sales and production activities. At the moment, “there is less global and regional centralization of treasury functions by Hong Kong and mainland Chinese MNCs”, Badenach points out. “Assuming they will follow the trend of global MNCs over the last 10-15 years towards optimization of cash and liquidity, better control over treasury-related risks and streamlining of transaction processing, we may expect a trend towards centralization of their treasury functions.”

At present, Singapore may be the preferred destination for corporate treasury centralization. But on February 25, Hong Kong declared itself a serious alternative.

.jpg)