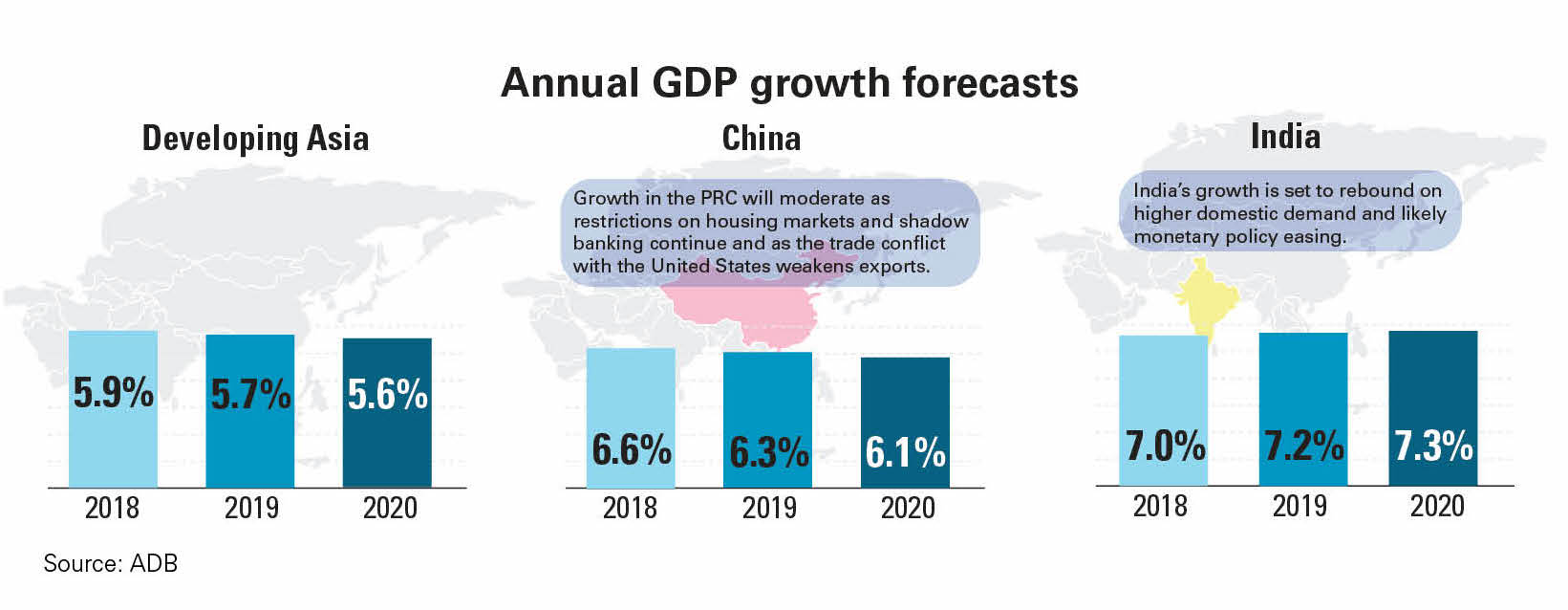

The latest Asian Development Outlook 2019, the flagship economic publication of the Asian Development Bank (ADB), forecasts that growth in the region will soften to 5.7% in 2019 and to 5.6% in 2020 – down from the 5.9% growth rate achieved in 2018.

Excluding the newly-industrialized economies of Hong Kong, China, Korea, Singapore and Taiwan, developing Asia is also projected to post a lower economic growth rate of 6.2% in 2019 and 6.1% in 2020, compared with 6.4% in 2018.

.jpg) ADB chief economist Yasuyuki Sawada says uncertainty clouding the economic outlook remains elevated. But he points out growth overall remains solid with domestic consumption strong or expanding in most economies around the region. “This is softening the impact of slowing exports,” he adds.

ADB chief economist Yasuyuki Sawada says uncertainty clouding the economic outlook remains elevated. But he points out growth overall remains solid with domestic consumption strong or expanding in most economies around the region. “This is softening the impact of slowing exports,” he adds.Sawada says risks remain tilted to the downside. A protracted or deteriorating trade conflict between China and the US could undermine investment and growth in developing Asia. With various uncertainties stemming from the US fiscal policy and a possible disorderly Brexit, growth in the advanced economies could turn out slower-than-expected, impairing the outlook for China and other economies in the region.

China will likely see economic growth moderate to 6.3% in 2019 and to 6.1% in 2020 from 6.6% in 2018. This is against the backdrop of structural changes in the economy, shifting from industry and towards services, as well as in the financial tightening as the government seeks to control financial risks by reducing corporate leveraging.

.jpg) “It is natural for an economy like China, which has successfully achieved middle income status and manifests continuous development, to experience a moderate growth rate,” explains Sawada.

“It is natural for an economy like China, which has successfully achieved middle income status and manifests continuous development, to experience a moderate growth rate,” explains Sawada.Going forward, the main risk to China’s growth outlook is the possible escalation of the trade conflict with the US, which would damage investor and consumer sentiments. The domestic downside risk include policymakers seeing measures to stabilize growth as insufficient – thus abandoning efforts to stabilize local lending, or loosening restrictions on shadow banking and allowing debt from non-bank financing to increase.

“The Chinese economy remains strong despite the growth slowdown in recent years,” notes Sawada. “Although the slowing trend will likely persist if the trade uncertainty continues, favourable fiscal reforms at the start of the year, particularly on personal income tax and social security, will help alleviate the adverse effects of anticipated weaker wage growth and boost domestic consumption.”

ADB argues the need to reform the social security contributions as a key policy challenge to China. To address this, the government should tackle the under reporting of pension contributions, the inefficient collection of social security contributions and legacy costs from obligations to retirees who become eligible for state pensions when the pension system was modified in 1997.

Consumption will remain the main growth driver for the Chinese economy in coming years, although it is expected to slacken slightly as the household income growth subsides. In 2018, consumption contributed five percentage points to the country’s GDP, while household consumption expenditure rose 6.2%.

ADB says a gradual loosening of local housing market restrictions in 2019 will boost property-related consumer spending and support retail sales in the latter part of this year and the next.

On China’s labour market, the outlook is less robust. ADB notes that slower consumption and foreign investment due to the ongoing trade tensions will dampen demand for low-skilled and blue-collar workers. This comes as the country’s unemployment rate has risen from 4.9% in December 2018 to 5.3% in February 2019.

Meanwhile, price inflation in China will remain benign at 1.9% in 2019 and 1.8% in 2020 on the back of declining domestic growth, lower global oil prices, a stable Chinese renminbi against the US dollar and sharply lower producer prices.

The Chinese government’s monetary policy is expected to become more accommodative in 2019, with the central bank continuing to cut the bank reserve requirements ratio. An expansionary stance towards fiscal policy, which started in the second half of 2018, will also continue this year.

In contrast to China, India’s economy will register higher growth rate in the next two fiscal years, getting a lift from the recent policy measures by the government, which will improve the investment climate and boost private consumption and investment.

ADB forecasts India’s GDP growth to rise to 7.2% in fiscal year (FY) 2019 ending March 31 and to 7.3% in FY2020, reversing the two years of declining growth as a result of reforms to improve the business and investment climate.

“India will remain one of the fastest-growing major economies in the world this year given the strong household spending and corporate fundamentals,” Sawada points out. “India has a golden opportunity to cement recent economic gains by becoming more integrated in the global value chains. The country’s young workforce, an improving business climate and a renewed focus on export expansion all support this.”

“India will remain one of the fastest-growing major economies in the world this year given the strong household spending and corporate fundamentals,” Sawada points out. “India has a golden opportunity to cement recent economic gains by becoming more integrated in the global value chains. The country’s young workforce, an improving business climate and a renewed focus on export expansion all support this.”What will boost household income, according to ADB, includes income support to farmers, hikes in procurement prices for food grains and tax relief to taxpayers earning less than 500,000 rupees (US$7,212). Declining fuel and goods prices are also expected to provide an impetus for consumption. An increase in utilization of production capacity by firms, along with falling levels of stressed assets held by banks and easing of credit restrictions on certain banks is expected to help investment grow at a healthy rate.

.jpg) But downside risks persist, including a higher-than-expected moderation in global demand and a potential intensification of trade tensions. Lower-than-targeted tax revenues or a delay in strengthening bank and corporate balance sheets could also undermine India’s economic expansion.

But downside risks persist, including a higher-than-expected moderation in global demand and a potential intensification of trade tensions. Lower-than-targeted tax revenues or a delay in strengthening bank and corporate balance sheets could also undermine India’s economic expansion.Consumer price inflation is expected to rise to 4.3% in FY2019 and 4.6% in FY2020 as food costs increase slightly and domestic demand strengthens. Given that inflation is expected to average around 4% in the first half of FY2019, the central bank will have some room to lower the policy rates.

Imports are expected to increase mainly due to strong domestic demand while a growth slowdown in India’s key export destinations would affect export growth. The current account deficit is projected to widen a bit to 2.4% of GDP in FY2019 and to 2.5% in FY2020. But this does not pose any immediate challenge as the shortfall is expected to be funded comfortably by capital flows, given that India has emerged as an attractive destination for foreign investment.

A key factor driving India’s persistent current account deficit is its lukewarm export performance compared to other East Asian and Southeast Asian economies. India’s export performance could benefit from greater participation in global value chains (GVCs).

What could help India integrate more with GVCs include lower trade costs, improved infrastructure quality and enhanced worker skills. Global experience, according to ADB, suggests that enhanced GVC participation is also associated with other development goals that India strives to achieve such as higher economic growth, an increase in the share of manufacturing in GDP and faster job creation.

In other regions, ADB says Southeast Asia will witness a weaker growth rate of 4.9% this year and 5% in 2020, compared with 5.1% in 2018. Export demand is likely to soften in 2019 in line with the weaker global environment and a muted forecast for semiconductor exports, before picking up slightly in 2020.

Strengthening domestic demand will offset the weaker growth, while strong consumption, spurred by rising incomes, subdued inflation and robust remittances, should boost economic activity in the region.

.jpg)

.jpg)