Family-owned corporations have earned a bad rap in the investment community amid a popular view that those who run them tend to be more interested in maintaining control over the business than in enhancing efficiency and growth, and as such have been seen as less receptive to calls for transparency and accountability.

However, Credit Suisse Research Institute (CSRI), the Swiss banking group's in-house think tank, says in its latest report that family-owned businesses have continued to outperform their non-family-owned peers in every region and sector while showing greater resilience amid the Covid-19 pandemic.

That's because family-owned businesses pursue a longer-time horizon in their investment strategy, delivering more stable and superior through-cycle profitability, and ultimately driving significant excess returns for all shareholders, according to the report, titled ”Credit Suisse Family 1000: Post the Pandemic”.

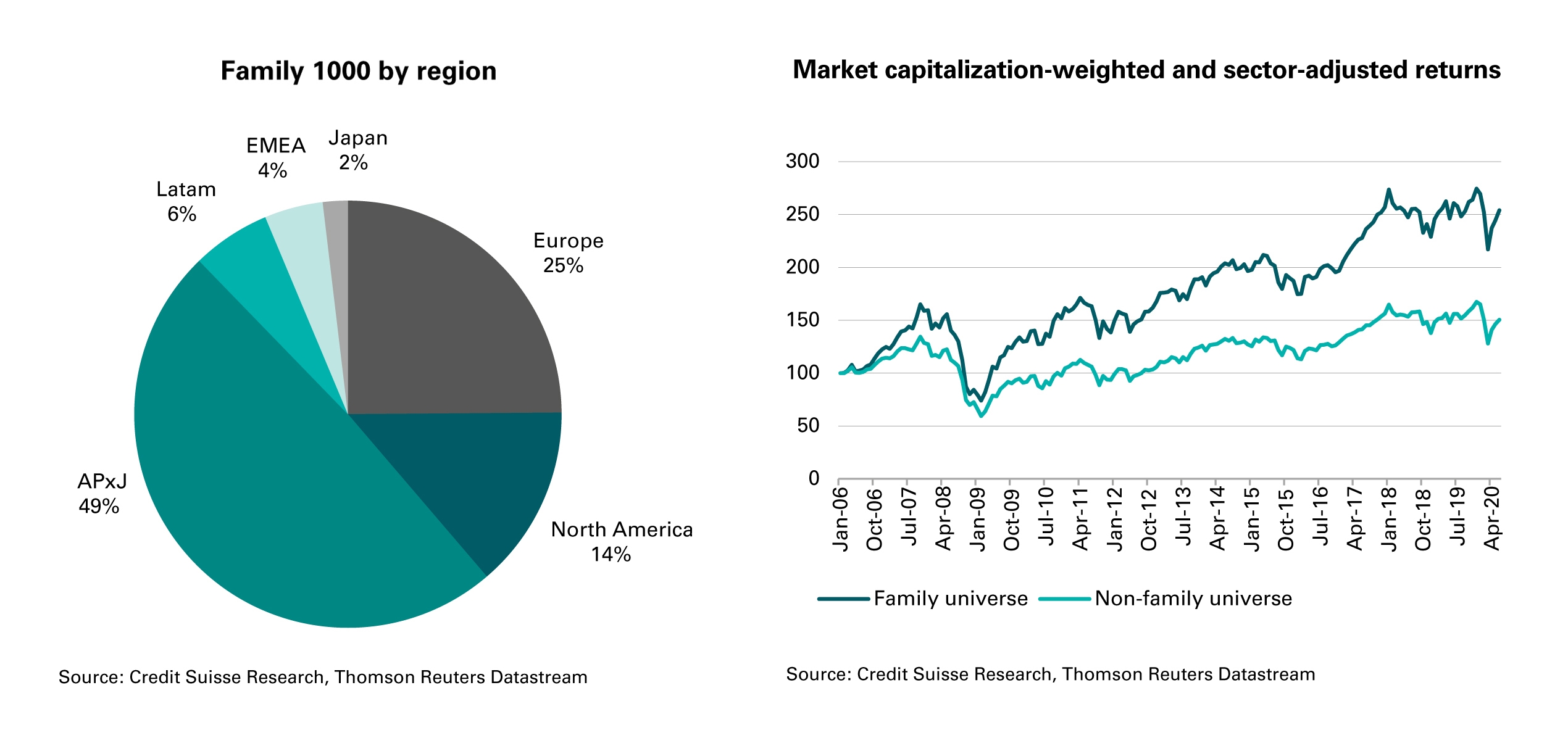

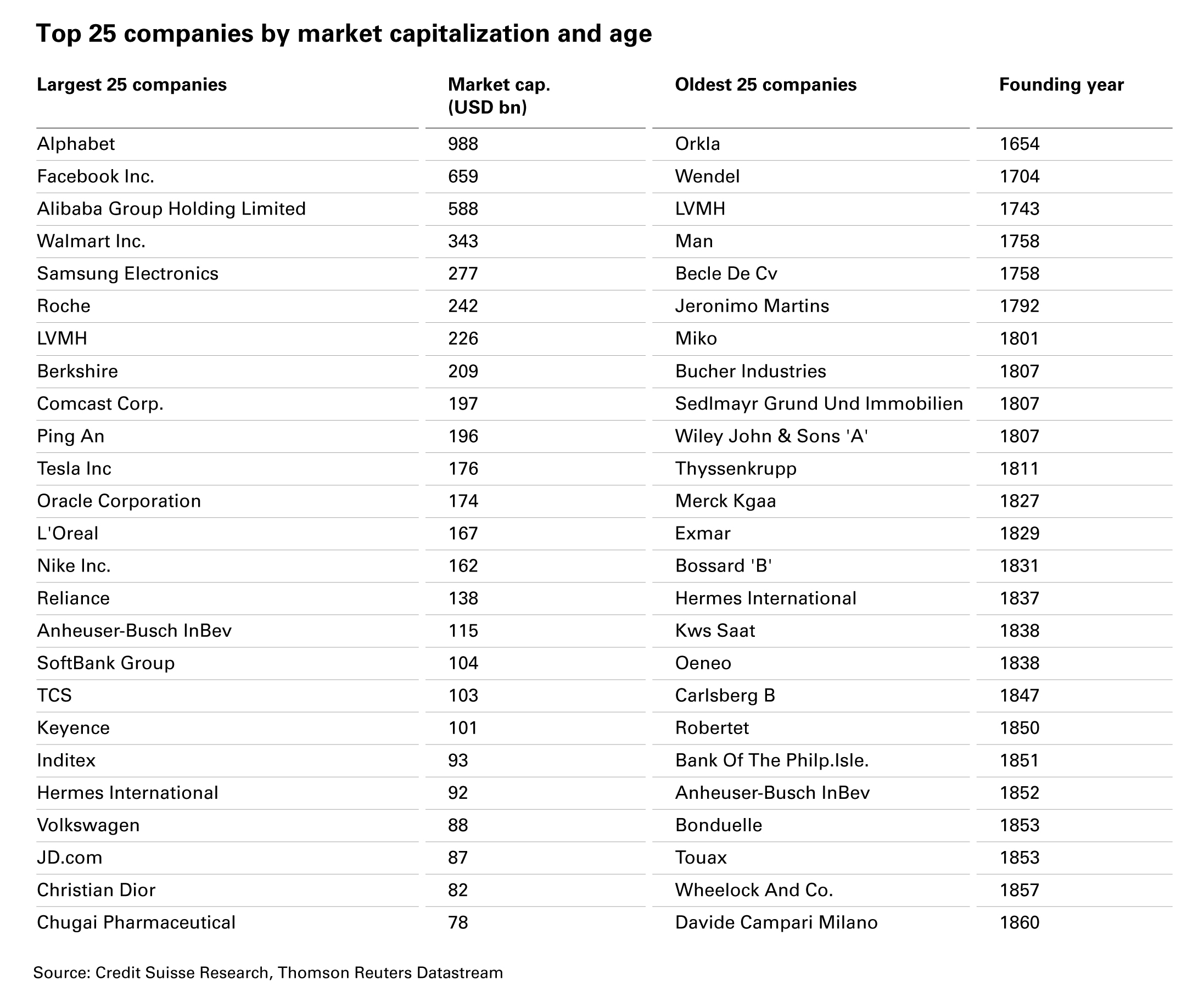

Using its proprietary database of more than 1,000 publicly listed family- or founder-owned companies, CSRI has found that since 2006, the overall “Family 1000” universe has outperformed non-family-owned companies by an annual average of 370 basis points. Asia Pacific (APAC) ex-Japan has seen the most pronounced effect, with compound excess returns of more than 500bp per annum, followed by Europe, at 470bp.

(The database consists of firms that meet one or both of the CSRI criteria for family ownership: the founder or their family owns at least 20% of the company’s share capital, and the founder or their family controls at least 20% of the company’s voting rights.)

In Asia Pacific including Japan, the report covered 12 markets that continue to dominate and represent a 51% share of the universe, with a total of 540 companies and a market capitalization of over US$5.56 trillion. These include 159 family-owned companies in China with US$2.48 trillion in total market capitalization and 71 family-owned firms in Hong Kong with a combined market cap of US$505.1 billion. Together with the 111 family-owned companies in India, the three jurisdictions comprise 63% of the APAC region, with a combined market capitalization of US$3.9 trillion, or 70% of the regional market.

The pandemic has had a significant impact on equity market returns and volatility in 2020. Family-owned companies tend to have above-average defensive characteristics that allow them to perform well, particularly during periods of market stress. Data for the first six months of this year supports that view, given an overall year-to-date outperformance of around 3% relative to non-family-owned companies. This outperformance was strongest in Europe and APAC ex-Japan, at 6.2% and 5.1% respectively. Family-owned companies in Japan outperformed their non-family-owned peers by 30.1% during the period.

Greater profitability

The report suggests that, since 2006, revenue growth generated by family-owned companies has been more than 200bp higher than that of non-family-owned firms. At the same time, analysis of the data indicates that family-owned companies tend to be more profitable. For example, average cash flow returns are around 200bp higher than those generated by non-family-owned firms. These superior returns are observed across all regions globally.

As regards environmental, social and governance issues, family-owned companies on average tend to have slightly better ESG scores than their non-family-owned counterparts. This overall superior performance, which has strengthened over the past four years, is mostly led by higher environmental and social scores as family-owned companies appear to lag non-family-owned firms in terms of governance, says the report. European family-owned companies have the highest ESG scores. Family-owned companies in APAC ex-Japan are scoring better than those located in the US and their scores are rapidly converging with those generated by their European counterparts.

It has also been noted that older family-owned companies have better ESG scores than younger family-owned firms. The report says this is probably because the older companies have more established business processes in place, which allow them to incorporate or focus on areas of their business that are not directly related to production processes but are relevant in terms of maintaining overall business sustainability.

In order to better understand the ESG characteristics of family-owned companies, a survey of more than 200 companies was conducted. The companies were asked how much of a concern Covid-19 is to them going forward. Despite the impact on revenue growth this year, it seems that family-owned firms surveyed view Covid-19 as slightly less of a concern to their prospects than non-family-owned companies. Family-owned companies have also resorted less to furloughing their staff than non-family-owned companies (46% against 55%). Among family-owned companies, support programs have been set up most often in APAC ex-Japan rather than in Europe or the US. This might reflect a greater availability of government-sponsored support programs in these regions, says the report,

But while family-owned companies have focused more on social policies since the outbreak of the pandemic, they seem to lag non-family-owned peers on several ESG-related factors, most noticeably human rights and modern slavery-related policies. Family-owned companies on average have less diverse management boards, fewer of them have support groups for the lesbian, gay, bisexual and trans (LGBT) and black, Asian and minority ethnic (BAME) communities, or have made public statements related to United Nations principles, according to the CSRI report,

Says Credit Suisse group chairman Urs Rohner, who also chairs the research institute: “We have tracked the performance of family-owned businesses compared to non-family-owned businesses for many years now and have seen a regular pattern of stable and superior through-cycle profitability and returns for all shareholders, minorities included.”

Eugène Klerk, head of the bank's global ESG research product and author of the report, adds: “Our latest Family 1000 report reaffirms many of the outperformance metrics family-owned businesses have shown in our previous studies compared to non-family-owned businesses. When talking to investors about family-owned companies, we often hear that they outperform because of a perceived longer-term investment focus compared to non-family-owned companies. Our analysis suggests that this is indeed the case.

“This year, with the exceptional circumstances of a global pandemic, we delved deeper in our analysis and found that the traditionally more conservative financial model of family-owned companies built on lower leverage and stronger cash flow generation has proven to be an asset. They have notably relied less on government employment support to furlough their workforce, implicitly reflecting their own social responsibilities.”