The introduction of new corporate fund structures by Hong Kong, Australia and Singapore (the OFC, CCIV and VCC respectively) is designed to encourage asset managers to look at domiciling funds in the fast-growing Asia Pacific region. Yet each vehicle goes about doing so differently, and that makes deciding between them a complex task. Our extensive asset servicing experience in supporting comparable schemes, such as UCITS, allows us to assess each, and determine which may provide the best fit with fund managers’ strategic goals and investment strategies.

In this two-part series, we outline the background, key features and the issues asset managers should consider when deciding whether to use these new structures in their fund manufacturing and distribution strategies.

Getting to grips with OFC, CCIV & VCC

Asset managers need to consider a number of factors, including regulatory, competitive and investor demands, when considering where to domicile their investment fund offerings.

In APAC, where assets are forecast to double from their 2016 levels to nearly USD 30 trillion by 20251, Australia, Singapore and Hong Kong are looking to further build and reinforce their positions as regional asset management hubs. Regional governments and regulators are committed to attracting investment, increasing cross-border trade and regulatory cooperation to create a dynamic and globally competitive funds management industry. The introduction of the new corporate structured fund vehicles in Asia Pacific offers a credible and compelling offering.

The introduction of these new fund structures also comes at a time of increased efforts to develop a single regional market for funds through various cross-border passporting schemes - notably, the ASEAN Collective Investment Scheme (ASEAN CIS)2, the Asia Region Funds Passport (ARFP)3and various bilateral schemes such as the Hong Kong- China Mutual Recognition of Funds (MRF) scheme4.

More choice, greater flexibility

The new structures introduce some important benefits, such as allowing an umbrella and sub-fund structure, and reduce some compliance requirements. Part two of this series assesses some of the advantages and disadvantages of each, as well as the ancillary factors driving fund managers (and investors) to consider them.

This article outlines the basics behind:

- Hong Kong's Open-ended Fund Company (OFC), which launched in 2018.5

- Singapore's Variable Capital Company (VCC), which is expected to launch later in 2019.6

- Australia's Corporate Collective Investment Vehicle (CCIV), which was expected to launch in 2019, but now looks likely to launch in 2020.7

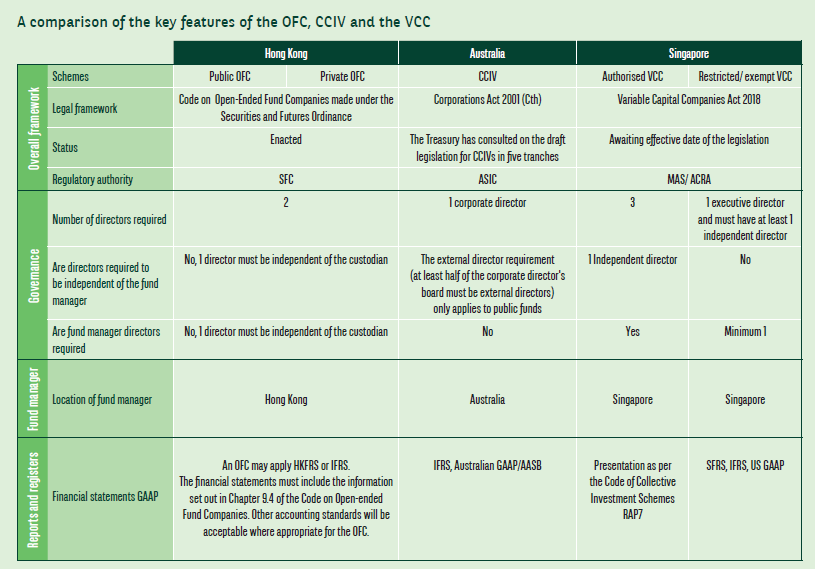

Hong Kong's OFC

Hong Kong’s mutual funds have not been able to accommodate diverse needs from fund providers, though its laws have long allowed asset managers to set up investment funds in a unit trust structure. The OFC allows them to set up under a corporate structure.

Unlike a unit trust structure, the OFC does not require a trustee, but acts for and on behalf of itself. Additionally, its enabling law – the Securities and Futures Ordinance – permits it a variable capital structure, which is not the case with companies formed under the Companies Ordinance8.

Cost-wise there is little difference between the OFC and the unit trust structures. However, if we compare the cost of selling the funds established in Hong Kong versus outside Hong Kong, there is a cost benefit to set up as an OFC: An OFC is simpler and cheaper because it only requires compliance with Hong Kong legislation.

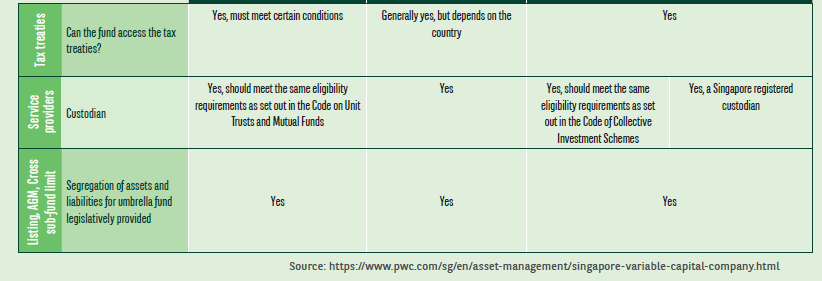

An OFC can have an umbrella and sub-funds structure, and the law supports cross-investment of sub-funds. It can be public or non-public, and must have a board of directors with at least two individual directors. It must appoint a fund manager, an external auditor, and a custodian who has responsibility for all safekeeping of assets.

A key benefit promoted by the authorities is that being domiciled in Hong Kong provides access to mainland China, although whether or not the OFC funds will be distributable under the MRF scheme has not yet been clarified9.

Singapore's VCC

This specialised corporate structure introduces a fourth fund type to Singapore and is designed to provide fund managers with greater operational flexibility and help them reap economies of scale and monetary savings.

The enabling law (the Variable Capital Companies Act 2018) supports umbrella and sub-funds structures, with sub-funds able to appoint a local board of directors and use the same service provider as the umbrella fund.

A VCC covers both traditional and alternative assets, can be open-ended and closed-ended, and can be used for retail and non-retail strategies10. A retail fund requires three directors; a non-retail fund requires one.

Singapore’s strategic positioning in the region and its role as one of the world’s most competitive nations should further attract interest from asset managers11.

Australia's CCIV

With the largest fund management industry in the Asia Pacific region, the introduction of the CCIV could prove to be a boon for the country12.

CCIVs have a range of benefits: they have an internationally recognised corporate structure limited by shares; they are designed to integrate with the ARFP cross-border initiative; and they complement the existing regulatory framework, potentially creating cost efficiencies and reducing compliance costs.

In a first for Australia’s fund management market, a CCIV must have one sub-fund (and can have more). Additionally, sub-funds can offer a range of investment strategies delivering increased investor choice, scale and cost-savings.

To protect investors, sub-funds’ assets and liabilities must be kept separately, with each CCIV required to have an authorised corporate director, which must be a public company. It is expected that the law will permit both retail and wholesale CCIVs and introduce a depositary requirement for retail CCIVs.

The second part of this series looks more closely at some of the factors that fund managers and investors should consider with funds that use these new structures, and their prospects for success.

Thanks to our Asia Pacific footprint and global cross-border expertise, BNP Paribas can help clients to identify the impact of the different schemes from a cost of administration or ability to support different investment strategies perspective. We provide support from set-up with trustee, custody and transfer agency services, as well as fund administration.

Call our experts for a more in-depth conversation about cross border fund distribution.

Read more on the benefits, drawbacks and challenges to consider in Part 2 here.

1 Asset & Wealth Management Revolution: Embracing Exponential Change, PwC (2017). See: https://www.pwc.com/gx/en/asset-management/asset-management-insights/assets/awm-revolution-full-report-final.pdf

2 For more, see: ASEAN Collective Investment Scheme (ASEAN CIS) - regulation memo, BNP Paribas Securities Services (April 24, 2019). See: https://securities. bnpparibas.com/insights/asean-cis-collective-investment.html

3 For more, see: Asia Region Funds Passport (ARFP) - regulation memo, BNP Paribas Securities Services (April 29, 2019). See: https://securities.bnpparibas. com/insights/arfp-asia-region-funds-passport.html

4 For more, see: Hong Kong Mutual Recognition of Funds (MRF) - regulation memo, BNP Paribas Securities Services (April 29, 2019). See: https://securities. bnpparibas.com/insights/hong-kong-mutual-recognition.html

5 FSFC implements open-ended fund companies regime, Hong Kong Securities and Futures Commission (27 Jul 2018). See: https://www.sfc.hk/ edistributionWeb/gateway/EN/news-and-announcements/news/corporate-news/doc?refNo=18PR90

6 Explanatory Brief on the Variable Capital Companies (Miscellaneous Amendments) Bill, Monetary Authority of Singapore (Aug 5 2019): https://www. mas.gov.sg/news/speeches/2019/explanatory-brief-on-the-variable-capital-companies-miscellaneous-amendments-bill-on-5-august-2019

7 For more, see: Australia Corporate Collective Investment Vehicle (CCIV) - regulation memo, BNP Paribas Securities Services (March 10, 2019). See: https://securities.bnpparibas.com/insights/result/cciv-regulatory-memo. html

8 For more, see: Hong Kong Open-Ended Fund Company (OFC) – regulation memo, BNP Paribas Securities Services (March 6, 2019). See: https://securities. bnpparibas.com/insights/ofc-regulatory-memo.html

9 “Hong Kong, Singapore Gear Up Reform in Asset Management Sector”, Regulation Asia (October 4th 2018). See: https://www.regulationasia.com/hong-kong-singapore-gear-up-reform-in-asset-management-sector/

10 For more, see: The Singapore Variable Capital Company – regulation memo, BNP Paribas Securities Services (February 12, 2019). See: https://securities. bnpparibas.com/de/insights/vcc-regulatory-memo.html

11 The Global Competitiveness Report 2018, World Economic Forum See: http://www3.weforum.org/docs/GCR2018/05FullReport/ TheGlobalCompetitivenessReport2018.pdf

12 For more, see: Australia Corporate Collective Investment Vehicle (CCIV) – regulation memo, BNP Paribas Securities Services (March 10, 2019). See: https:// securities.bnpparibas.com/insights/result/cciv-regulatory-memo.html

Disclaimer

BNP Paribas Securities Services is incorporated in France as a partnership limited by shares and is authorised and supervised by the ACPR (Autorité de Contrôle Prudentiel et de Résolution) and the AMF (Autorité des Marchés Financiers).

The information contained within this document (‘information’) is believed to be reliable but neither BNP Paribas Securities Services nor any of its related entities warrant its completeness or accuracy nor accept any responsibility to the extent that such information is relied upon by any party BNP Paribas Securities Services shall not be liable for any errors, omissions or opinions contained within this document. Opinions and estimates contained herein constitute BNP Paribas Securities Services' or its related entities’ judgment at the time of printing and are subject to change without notice. This document is not intended as an offer or solicitation for the purchase or sale of any financial product or service. The information contained in this document does not constitute financial advice, is general in nature and does not take into account your individual objectives, financial situation or needs. You should obtain your own independent professional advice before making any decision in relation to this information. The information contained in this document is not intended for retail investors. Any information contained within this document will not form an agreement between parties. BNP Paribas Securities Services ARBN 149 440 291 (AFSL No: 402467) has been registered in Australia as a foreign company under the Corporations Act 2001(Cth) and is a foreign ADI within the meaning of s 5(1) of the Banking Act 1959. This document is not intended as an offer or solicitation for the purchase or sale of any financial product or service outside of Australia and is intended for ‘wholesale clients’ only (as such term is defined in the Corporations Act 2001 (Cth)).

BNP Paribas Securities Services, acting through its Hong Kong Branch, is regulated by the Hong Kong Monetary Authority and is licensed by the SFC to conduct Type 1 (dealing in securities) regulated activity.

BNP Paribas Securities Services, acting through its Singapore Branch, is regulated by the Monetary Authority of Singapore.

The New Zealand securities services business operates through BNP Paribas Fund Services Australasia Pty Ltd. BNP Paribas Fund Services Australasia Pty Ltd is a wholly owned subsidiary of BNP Paribas Securities Services. BNP Paribas Fund Services Australasia Pty Ltd ABN 71 002 655 674 (‘BPFSA’) is an Australian incorporated company which is registered with the New Zealand Companies Office under registration number 1010736. BPFSA is also registered under the Financial Service Providers (Registration and Dispute Resolution) Act 2008.