Private equity (PE) is expected to sustain its strong momentum in 2021 after bouncing back in the second half of last year following a slowdown in deal activity during the first half in the wake of Covid-19.

Despite the pandemic, there were several notable trends from last year, including increasing allocations to alternative assets – specifically PE and venture capital (VC) – with the amount of “dry powder”, or committed but unallocated capital, growing at 22% over the 2019-2020 period, according to data from Prequin.

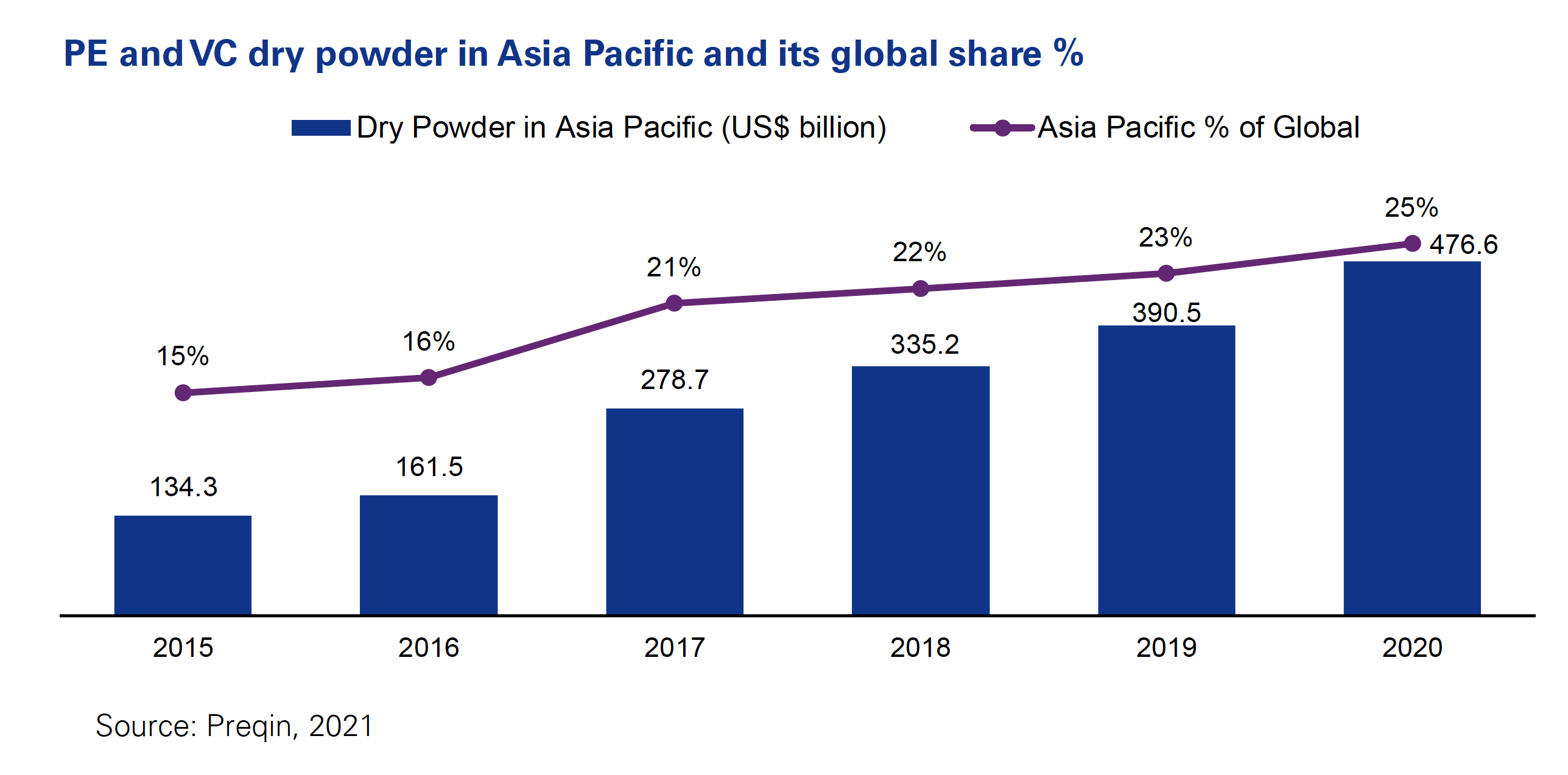

Asia-Pacific PE and venture capital (VC) dry powder has reached a record level of more than US$476 billion as of November 2020. The region’s PE/VC dry powder market share now represents 25% of the global total, well above Europe’s 19%.

“Deal activity continues to benefit from the low interest rate environment. We expect dry powder allocated to the region to continue to outgrow the US and EMEA in 2021 as institutional investors continue to increase allocations toward Asia PE/VC,” says Andrew Weir, global chair of asset management and real estate; regional senior partner and vice chairman, at KPMG.

Capital raising remains robust with successful general partners (GPs) benefiting from the ability to raise large Asia dedicated funds. Reported examples include KKR’s US$13.1 billion Asian Fund IV (to date the largest pan-Asian PE fund); GL Ventures at US$1.4 billion; and Baring’s US$6.5 billion BPEA Fund VII (its largest fund to date).

“Sectors such as education, logistics, healthcare and technology saw strong demand as they benefited from structural changes due to the pandemic. We expect continued momentum in 2021 within these business models and others that benefit from the new environment,” Weir says.

Long-term trends

This outlook was echoed by Stephen Catherwood and Ashmi Mehrotra, co-heads of private equity group at J.P. Morgan Asset Management, who say: “Overall, we continue to have a positive outlook for private equity despite an increasingly competitive market environment. Long-term trends, particularly in the area of technology and innovation, are creating opportunities for disciplined, experienced managers to generate attractive returns.”

Co-investments offer limited partners (LPs) the opportunity to invest directly in individual private companies alongside a GP that leads due diligence and is ultimately responsible for executing the deal, according to Catherwood and Mehrotra.

Relative to other types of private investment opportunities, co-investments have the potential to provide return enhancement (net returns enhance the portfolio), attractive economics (no-fee, no-carry basis), and increase visibility and discretion.

“Research shows that co-investment net returns can enhance overall private equity portfolio performance although selection is critical as greater upside potential comes with a higher dispersion of outcomes. For LPs, the majority of co-investments are made on a no-fee, no-carry basis. Also, co-investments are offered as pre-identified opportunities, not on a blind pool basis, as is the case in PE commingled funds,” Catherwood and Mehrota say.

Smaller deals

In 2021, investors would do well to look at smaller deals which can deliver differentiated results instead of going after the bigger, often more prominent, deals.

“While the largest buyout deals tend to grab headlines, we see the most attractive opportunities among firms with revenues of US$10 million to US$100 million. Despite increasingly competitive markets, these businesses can generally be purchased at lower valuation multiples with transaction structures less reliant on leverage,” say Catherwood and Mehrota.

“Smaller, undermanaged companies, even when fundamentally sound, can often benefit tremendously from collaboration with experienced general partners that have the deep sector expertise to drive transformational change. Once a growth plan has been successfully implemented, these businesses can be sold at premium valuations and drive differentiated returns for investors.”