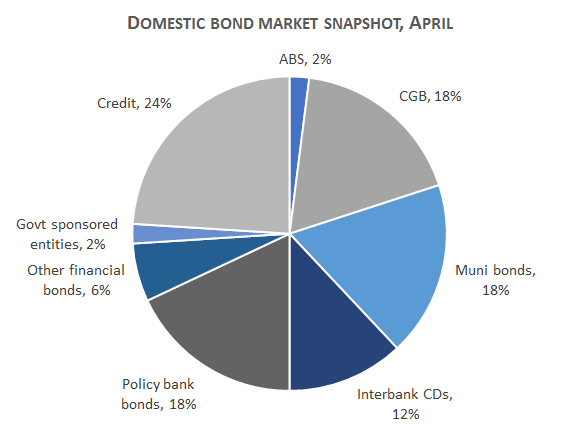

The domestic renminbi bond market expanded by 6.7% or 4.5 trillion renminbi (US$663.72 billion) in the first half of 2017 driven primarily by the net financing of commercial banks and local government for fiscal and debt swap, which accounted for 40% and 39%, respectively, of the overall net market supply.

A China bond market update issued by Deutsche Bank shows net financing by policy banks and other financial institutions accounted for 13% of the market, while the central government (CGB) contributed 10%. Net issuance by asset-backed securities and bonds by government-sponsored entities accounted for another 6%. On the other hand, the corporate credit market suffered from net redemptions of 358 billion yuan in the first half of this year.

In June, the report says government financing remained strong, while the interbank certificate of deposit (CD) financing staged a rebound. However, corporate direct financing continued to struggle due to the persistently unfavourable market environment.

After a temporary slowdown during April-May, the net issuance of interbank CD recovered in June to 419 billion yuan, from 359 billion yuan in May. The sizeable interbank CD issuance, the report points out, reflects a number of factors, including the strong seasonal interbank funding demand by commercial banks for quarter end and macro prudential assessment (MPA).

Source: Deutsche Bank bond market update

It was also due to the recovery of investment demand by money market funds and to the decline in interbank CD funding costs – by over 30bp for one-year term – thanks to the People’s Bank of China’s liquidity accommodation towards the end of June.

Net municipal bond supply in the first half of 2017 was about 1.8 trillion yuan, of which 27% was for local government debt swap – implying only 17% of the planned local government debt swap was completed in the first half. Deutsche Bank expects the government financing to accelerate in the third quarter of the year.

Corporate credit issuances remain sluggish as the market recorded net redemptions of 44 billion yuan in June – although it was less than what it was in May. The report says the lack of primary financing by the corporate sector can be attributed to elevated funding cost, weak appetite for corporate credit risk amid credit default events and fear of corporate event risks following the review of bank loans of privately-owned enterprises. The corporate credit sentiment is expected to remain vulnerable during the third quarter of the year.

In the interbank market, the asset management funds made a strong comeback in June, following net selling in May with net purchase of 802 billion yuan worth of bonds. Commercial banks bought 445 billion yuan net, or 37% of the market.

Deutsche Bank believes the launch of Bond Connect programme and the broad stability in money market conditions are supportive to asset allocation in the renminbi bond market in July and the third quarter of the year.