CHINA'S equity capital market has seen increasing interest from Taiwanese corporates over the past 15 months. In order to benefit from a larger market and higher P/E ratio, Taiwanese companies with mainland subsidiaries are increasingly looking to raise funds through China’s IPO market.

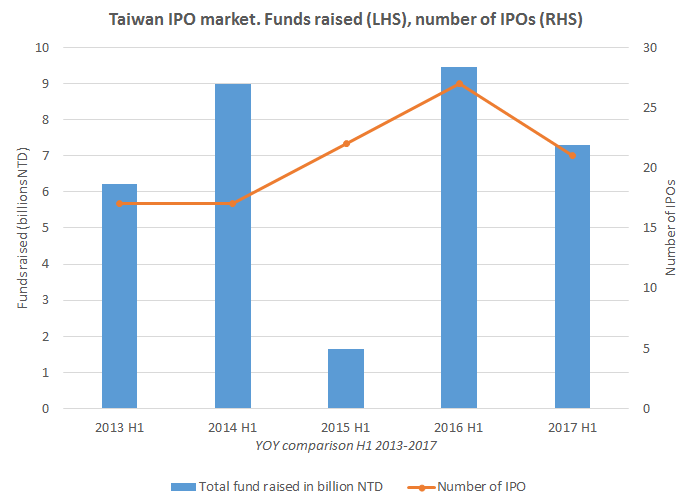

Since June of 2016, seven Taiwanese companies have completed debut IPOs in mainland China and Hong Kong, raising a combined total of US$438.78 million. To put into perspective, this is over half the amount raised through IPOs on the Taiwan Stock Exchange during the same period.

Following the seven successful deals, another Taiwanese corporate, Avary Holding, is also filing their A-share IPO. Currently, 26 Taiwanese companies are listed in the A-share market.

The high valuations that A/H share IPOs are able to achieve is considered the main driver of the rush. As of the end of July 2017, the P/E ratio of Taiwan listed stocks was 16.22, while the average P/E on the mainboard of SSE and SZSE was 16.98 and 35.75, respectively. The valuation gap is even larger for newly-listed companies.

From June 2016 to August 2017, the seven newly-listed Taiwanese companies in China and Hong Kong have seen an average increase of 134% in stock price, while during the same period newly-listed companies on the TSE only recorded average returns of 28%.

Another reason for the corporate flight is with respect to fundraising capability. Data from EY show that 246 companies completed IPOs in the A-share market in 1H17, raising US$19.25 billion. This is 79 times greater than the amount raised in the Taiwanese equity capital market.

From an investor’s perspective, unfriendly tax rates in Taiwan also deter them from participating in the secondary market. “In total, people need to pay up to 47% tax on cash dividends, which includes the maximum income tax rate of 45%,” says Allen Wu Jin Tang, executive vice president at Yuanta FHC. “Therefore, a lot of high net worth investors are withdrawing their money from the (Taiwanese) capital market. They don’t want to participate.”

In a 60-page report released in August, KPMG listed four major issues that Taiwanese corporates need to address in their A-share IPO applications: intra-group competitions, corporate restructuring, registration as a limited company, and employee compensation and benefits. According to KPMG, because China Securities Regulatory Commission sped up their IPO review in 2017, the chances of Taiwanese corporates getting approval will greatly improve.

In a bid to protect the Taiwanese IPO market, the Taiwan Stock Exchange issued modified regulations on overseas listings on August 22. The regulations require IPO decisions to be approved by the board of directors of the parent company.

In the meantime, the Taiwanese government is also trying to address tax issues. “People talked to the government, saying that if the capital market is performing so poorly, it causes difficulties for companies in Taiwan seeking IPOs or fundraising,” says Wu. “The government listened and tried to do something on cash dividends in May. In September, the government proposed a tax reform scheme. It is expected to be approved by the Legislative Yuan by the end of this year.”

For now, the new China rush is likely to persist for the rest of 2017. The first China rush for Taiwanese corporates started in 1987 when the Taiwanese government allowed Taiwanese citizens to visit their relatives in mainland China. Since then, a number of Taiwanese corporates have flooded into mainland China and set up factories to benefit from the lower cost of labour.

The story is an extract from The 6th annual Taiwan report, which will feature in the October edition of The Asset magazine. Please contact us for more details on obtaining a subscription.