As technology booms in China, young technology startups are able to get venture capital investment with little effort. However, easy cash, aggressive investment behaviour and poorly optimized cash flow have led to a poor state of financial health for some of China’s tech companies.

Take the recent troubles of Chinese technology conglomerate LeEco, which reflects the cash management difficulties faced by many technology startups. In late 2016, company chairman Jia Yueting wrote in a letter to employees that, “We blindly sped ahead, and our cash demand ballooned. We got over-extended in our global strategy. At the same time, our capital and resources were in fact limited.”

Since then, LeEco have had to restructure their debt, cut some of their business line, and implement changes in senior management. LeEco recently said in an official statement, somewhat surprisingly, that it will “never owe any creditors, including financial institutions and suppliers, any money.”

Compounding on LeEco’s problems, in early July a Shanghai court froze 1.24 billion yuan (US$180 million) worth of assets belonging to LeEco and its founder Yueting Jia. LeEco’s dispute is over unpaid interest on debt, and is with one of its largest creditors, China Merchants Bank. In a recent statement, LeEco admitted it would be postponing its July payroll to August.

LeEco is also being sued by US TV maker Vizio over a failed merger, who are seeking US$60 million in damages. Vizio claim that the acquisition was a front to give a positive impression of LeEco’s financial standing, and that LeEco executives fraudulently claimed the company was financially healthy whilst knowing it could not afford the US$2 billion transaction.

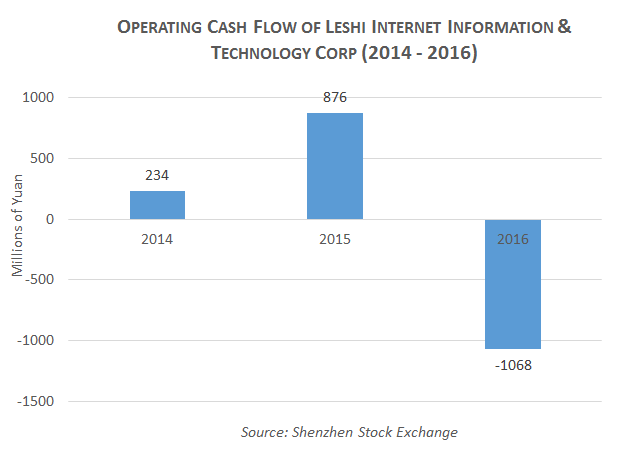

One of LeEco’s subsidiaries, Shenzhen-listed Leshi Internet Information & Technology Corp, said in an official statement that 99% of Jia’s stocks in Leshi have been pledged to banks as collateral to facilitate further borrowing, as it also experiences a significant drop in its own operating cash flow.

The cash crisis of LeEco, as many experts believe, is attributed to its unreasonably aggressive investment behaviour and its over-estimation of its own ability to generate cash. “As market liquidity gets tighter, the cash flow will definitely break because of its over-expansion and lack of profitable business,” says Ximiao Dong, head of research at Hengfeng Bank.

As China speeds up deleveraging its financial markets, financial institutions have become more cautious in providing loans and managing their risk exposure. It is likely that any type of default will trigger a ripple effect, such as banks repatriating loans. Corporates with high debts, as a result, are extremely vulnerable to this type of credit event.

Yidao Yongche, a ride-sharing company was unable to return cash deposits to its customers and drivers due to a shortage of cash earlier this year. Some local new energy vehicle manufacturers competing with Tesla have also made large losses and were unable to pay back their existing debts.

In the bike sharing market, one of the most promising industries in China, startups with poor cash flow have started to crash-out from the cash-burning competition. In mid-June, Wukong Bike, a Chongqing-based bike sharing company, announced that they have exited the market. This marks the first bike sharing company to pull back from the fierce cash-burning competition.

Successful Chinese tech unicorns, such as Didi and Xiaomi, have acquired cash management services from transaction banks. In 2016, China Merchants Bank provided a cross-border cash management solution for Didi, which streamlines the largest Chinese ride hailing company’s daily cash transactions.

Internet and technology companies often need heavy investment at the early stage of their business. Mostly, the cash raised from private investors is deployed for technological investments and distribution channels. A quick channel for cash flow will be necessary for such cash intensive industries.

Additional reporting by David Wingrove.