The Great Smog of December 1952 brought about by high-pressure weather systems and industrial pollution, mostly arising from the use of coal, attacked the respiratory system of Londoners over a five-day period, making over 100,000 ill and causing the death of over 12,000.

The event precipitated a change in public attitude towards air quality and galvanized the government to enact new regulations to tackle the problem. Importantly, the UK had the political will, resources and technology to accomplish the task at hand.

The world today is increasingly beset by similar events – searing heatwaves, uncontrollable wildfires, prolonged droughts, more destructive hurricanes and severe flooding, not to mention the current Covid-19 pandemic – all leaving misery in their path and all becoming part of a new normal.

Barriers

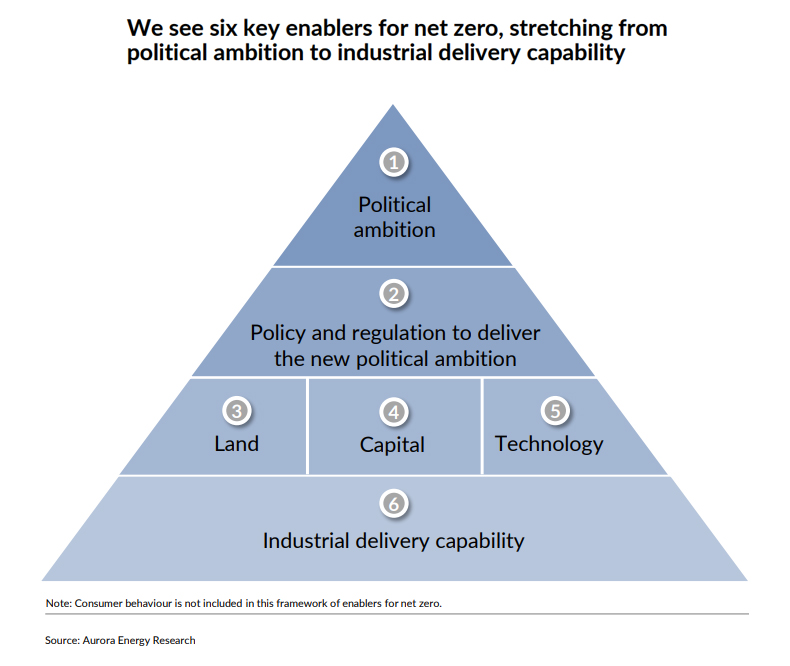

Efforts are being made to understand and combat this climate change trend. In a recent paper, UBS explored the six key enablers of energy transition1. Crucially, as with most things, it all starts at the top. The primary enabler is political ambition or a will to accomplish this task, that is, successfully combatting climate change.

As was the case in London in the 1950s, it must be accompanied by the correct policy and regulatory frameworks, the necessary resources (including capital and technology) and the capacity to do just that on an industrial and – in our case today – global scale.

Most or all of these enablers are available to us today, but, as we all know, there are a lot of moving parts and obstacles to overcome in order to progress. Not least of these obstacles, are the barriers put up and defended by those in some legacy industries (with much to lose in the short term), along with man-made climate change deniers.

Perhaps those that lead must step up to the plate and the reduction of human-induced climate change should become a clear unifying global objective. Most countries, according to a National Geographic 2019 article, are not on track to hit their 2030 Paris agreement climate goals or are not prepared for the “untold human suffering” that this failure will cause.

The more top-down or interventionist political systems may be a more fertile ground than other political systems for tackling the global issue of trying to limit the impact of climate change. If we believe that man-made climate change is an existential threat, then surely the main purpose of our governments should be to combat this.

The conditions in the more liberalized economies, with arguably shorter-term thinking due to the frequency of elections and powerful lobbying groups, may lead to a propensity to dilute the efforts aimed at combatting climate change. We now need swift and bold action before it is too late.

It is also worth noting that, in response to the pandemic, countries where trust in government and science, and in each other has been weakened, their economies have performed most poorly2.

Interestingly, while many might see that there are natural tensions between the public and private sectors of the economies, state and free-market systems, and East and West ideologies, a degree of convergence has come about, which is a positive development for the implementation of environmental, social and governance (ESG) goals.

China is moving from greater state control to a more liberalized economy, while Western economies look to regulation to protect the environment. The US is an important exception to this trend, although this might change depending on the results of the upcoming US election in November, which will provide a clearer picture of when oil demand will peak (if it hasn’t already done so) and where capex will go.

My hope is that we are now in a stream of such irresistible change – brought about by Covid-19, which has fostered a rejuvenated focus on personal health and the health of our planet – and that we are living through a paradigm shift when it comes to capital markets and the enabling of ESG factors.

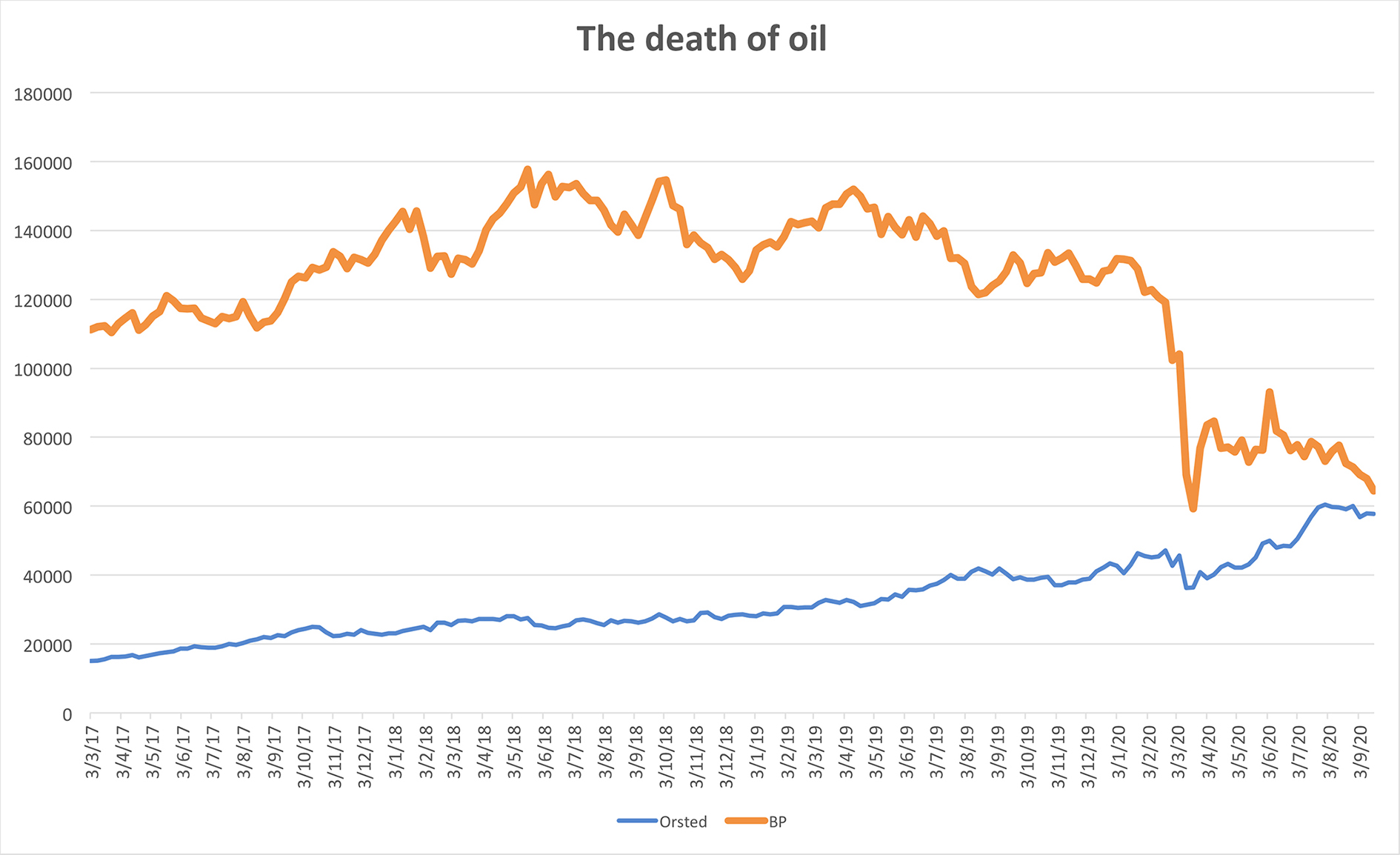

.jpg) The Covid-19 pandemic further consolidated my view on the relationship between human beings and climate change, and we have seen some remarkable phenomenon, such as the massive convergence of market capitalization between oil giant BP and a Danish renewable energy company (Orsted). Are we seeing the slow death of Big Oil? Has oil demand already peaked, or is it peaking sooner rather than later?

The Covid-19 pandemic further consolidated my view on the relationship between human beings and climate change, and we have seen some remarkable phenomenon, such as the massive convergence of market capitalization between oil giant BP and a Danish renewable energy company (Orsted). Are we seeing the slow death of Big Oil? Has oil demand already peaked, or is it peaking sooner rather than later?

Source: Bloomberg

Asia opportunity

Whether the timing of GAM’s decision to establish a separate Asia-focused bond strategy towards the end of 2019 – a mere few months before the pandemic – was good or bad, even with the benefit of hindsight, is subject to debate.

As a sustainability-minded individual, I see immense market opportunity. Aside from the breathtaking pace of growth, the Asian hard-currency credit market offers attractive relative value, low correlation and diversification, sound corporate fundamentals, favourable demographics and low-volatility.

Crucially, Asia provides ideal conditions for the take-off of the digital revolution, in which technology can change how energy is generated and how infrastructure can be built with much reduced reliance on capital and labour.

We have already seen how North Asia has benefited from its large share of the global consumer electronics supply chain and are now seeing how China’s political will has translated into dominance in the global solar power supply chain – alongside an ambitious plan to dominate the global electric vehicle supply and an aggressive target in green building.

Investing sustainably amidst the pandemic

Many decisions come with difficult debates. A recent challenge was considering my alignment to green bond taxonomy. Was it to be inclusive or exclusive?

The Climate Bond Initiative has a clear taxonomy to exclude fossil fuels and, hence, certain transition projects (for example, from coal-to-gas ones) are excluded from their certification programme. The Green Bond Principles (GBP), on the other hand, set out by the International Capital Market Association is more lenient, with a clear map between its GBP and the United Nations’ 17 Sustainable Development Goals.

I believe in an inclusive approach, it is more important to have a model in which everyone and every country can play a part in achieving the common goal, rather than a divided universe where climate change deniers end up owning all the fossil fuel assets.

Another challenge I faced in managing an Asian fixed-income credit fund was the mapping of quasi-sovereign corporates that carry a significant social mandate for their respective governments. There is no blueprint for this, even though the climate change debate has been on-going for decades. This step into the unknown has its own demands, especially when operating with a small, lean team.

One battle the GAM fixed-income team continues to fight is that of being underrated by external fund reviewers who do not have the capacity, methodology and data to take green bonds into account when rating bond funds.

This is despite the fact that the concept of “green bond”, invented more than a decade ago by the World Bank and the European Investment Bank, is considered the most prominent innovation of the last decade and has since channelled hundreds of billions of US dollars’ worth of capital into sustainable economic activity around the world.

There are those that still debate the desirability and ethics of short-term returns versus ESG goals. However, Covid-19 is making this an increasingly less relevant question. If ESG factors were relevant for a five-year investment horizon, pre-Covid 19, these factors are now being brought forward.

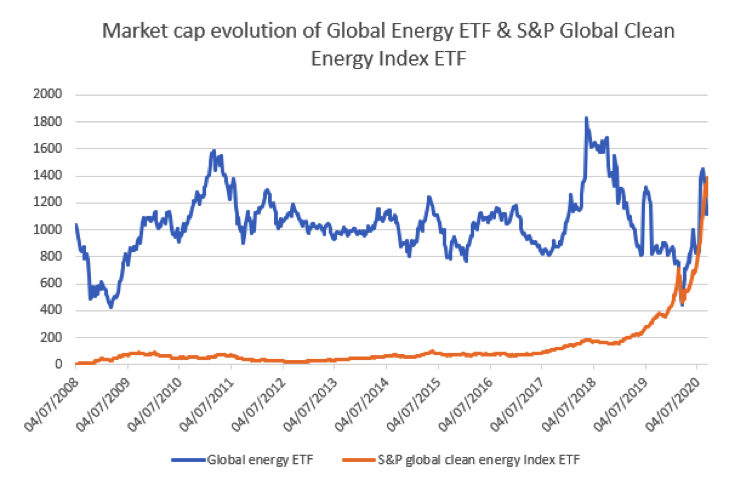

In other words, ESG considerations are increasingly more relevant and integrated in evaluating companies. One manifestation of this behavioural shift prompted by Covid-19 is the change in consumer preference towards clean energy ETFs – strong evidence that consumers are flexing their muscles, as the graph below illustrates.

Source: Bloomberg data, October 2020

Shifts like this allow critical mass to be reached and help resolve the chicken-or-egg dilemma, making ESG considerations more real and no longer just for disciples.

Glancing out of my window, seeing today’s youth and future returning from school, I’m drawn to reflect on my own life experiences. I spent my early formative years at the meeting point of rural and urban China. As a youngster, for most of the year I swam with my buddies in the clear local river.

As China moved through industrialization, the state of the river changed for the worse. Returning from university one vacation, I went to meet some old friends by the river. The next day, we all suffered from red, blotchy and itchy skin. Although this incident was more unpleasant than dangerous, it certainly made an impression.

We are only stewards of where we live, borrowing it from our children. While it might be an uncomfortable trade-off, nothing, not even China’s rush to lift millions out of poverty, should irreversibly and devastatingly impact the environment on our watch. As stewards of the environment, we should not only strive to improve our lot and the lot of others, but, now more than ever, seek to find ways of investing responsibly and sustainably.

Another positive sign, cited in a recent study, is the changing demographics of the global investor base that is increasingly including more women and millennials, both of whom have been showing a greater interest in stewardship.

.jpg) I’m happy to report that the economic development in my hometown over the last 20 years has been phenomenal and, in this case, the river is now clean again. And, like London with the Great Smog before, we can learn from our mistakes. It’s clear that we have reached the critical mass, there are enough people that recognize human-induced climate change exists. As a result, sustainable impact investing can improve returns and makes an increasingly measurable difference.

I’m happy to report that the economic development in my hometown over the last 20 years has been phenomenal and, in this case, the river is now clean again. And, like London with the Great Smog before, we can learn from our mistakes. It’s clear that we have reached the critical mass, there are enough people that recognize human-induced climate change exists. As a result, sustainable impact investing can improve returns and makes an increasingly measurable difference.

Amy Kam is the head of Asian credit at GAM Investments and is ranked as the number one astute investor in the UK-Europe region for 2020 by Asset Benchmark Research.

Related article: Asia’s top fixed-income investors, houses named

----

1“The State of the Global Energy Transition 2020", Arie et all.

2 Professor Joseph Stiglitz – “The Bottom Line” BBC Radio 4 – 10th October 2020.