As one of the region’s vibrant international financial centres, Hong Kong’s local currency bond market looks rather anemic. Issuances by the government make up ten times that of the rest of the market. Despite efforts by the Hong Kong Monetary Authority to create a bit more colour by introducing retail bonds and Islamic sukuks in recent years, the Hong Kong dollar bond market has so far failed to ignite the interest of especially local corporates.

The travails of the Hong Kong dollar bond market has not been helped by the rise of the offshore renminbi bond market (CNH), which until last year’s pullback saw a greater variety especially of high-yield issuers whetting the appetite of investors.

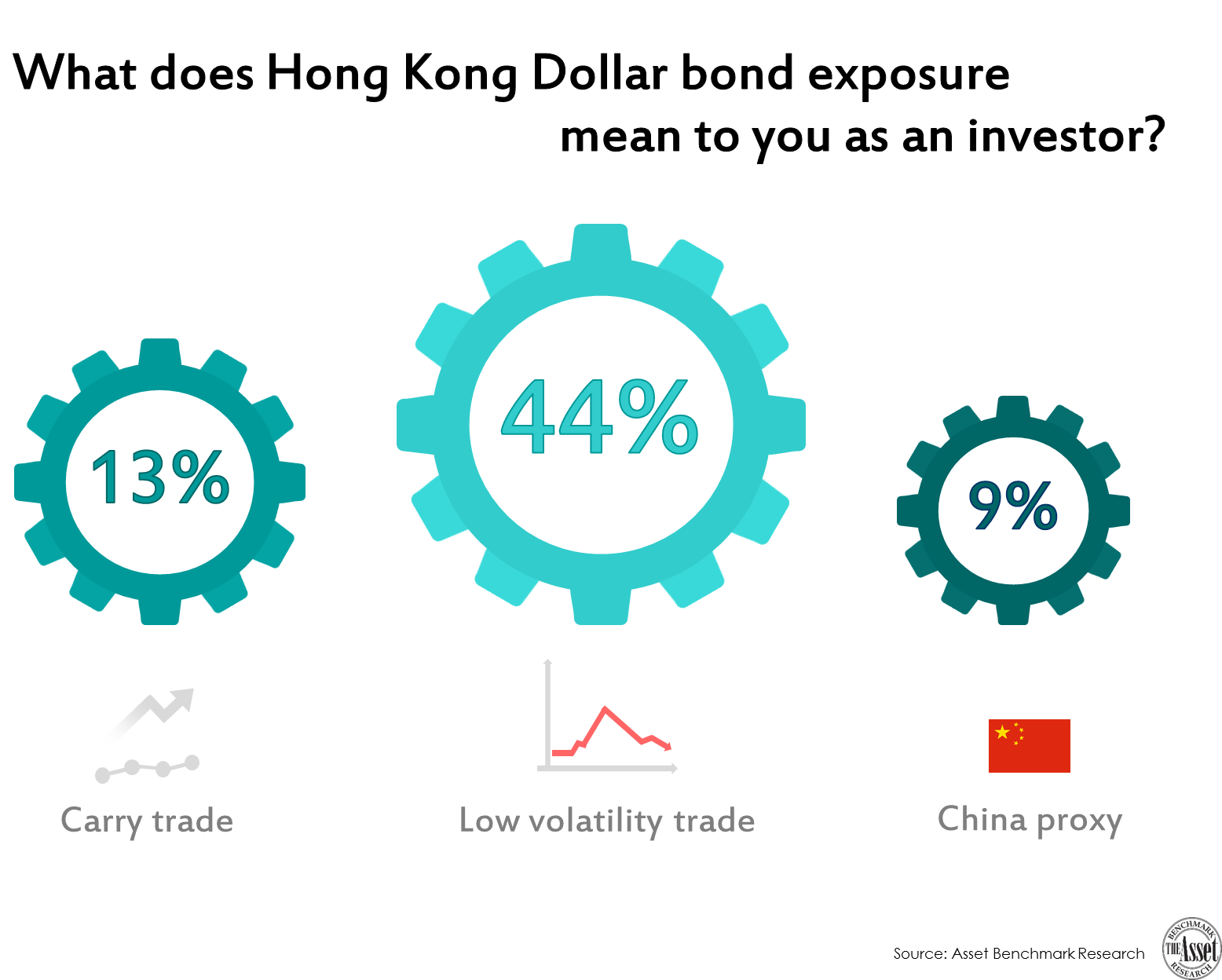

But there are still investors who see the value of investing in the US$320 billion Hong Kong dollar bond market. In an investor survey conducted by Asset Benchmark Research, 44% of respondents say they participate in the Hong Kong dollar bond market for its low volatility. Another 13% invest in Hong Kong dollar bonds as part of a carry trade. Only 9% say they see Hong Kong dollar bonds as a proxy for China.

“You have a situation where the government in Hong Kong has a surplus so they don’t need to borrow a lot of money,” explains Binay Chandgothia, a fund manager with Principal Global Investors. “That ensures that there’s not a lot of pressure on the yield curve for the government side of things.”

Chandgothia says that as Hong Kong is a net-savers market, there is always a lot of demand for long-term savings products from insurance companies, banks and asset managers. “There does not tend to be a prolonged sell-off. Even when sell-offs happen, they happen for a short period.”

But that idea that the Hong Kong dollar bond market is attractive for some investors because of the low volatility is not exactly the case, according to Ang Chow Yang, a fund manager with Schroder Investment Management. “It is probably because of less trading. As most Hong Kong dollar bond investors are of a buy-and-hold mentality, lower Hong Kong dollar indicative spreads movement underestimate the wider price discovery on actual trades,” he says.

Ang notes that in general the whole credit beta globally is still quite positive. “In fact, if anything over the past six months or so I think credit products are in large demand for a variety of reasons whether it is for the yield angle or investors are generally a bit more disenchanted with other risk asset classes such as equity given rising fears of secular stagnation.

Investors say the Hong Kong dollar bond market faces a number of challenges. “With Hong Kong dollar bonds, you don’t get very long-duration bonds,” says Chandgothia. “Most of the time, issuance tends to be five to 10 years. In the US, you actually get a much longer yield curve going out to 30 years. Even the Hong Kong government does not issue bonds that are longer than 15 years. Buying one is a struggle; the supply is tight.”

The Hong Kong market also does not have high-yield issuers as most corporate bonds are investment grade. “My feeling is most of the financing needs of the below investment grade issuers are fulfilled by banks through loans.” This is unlike in the CNH market where there are more high-yield issuances. “There is more volatility in the CNH market than in the Hong Kong dollar bond market,” notes Chandgothia. “Volatility can run both ways: it can be painful at times but it is also a way of enhancing returns if you are on the right side of it.”

The presence of more high-yield issuers in the CNH market is also one reason why Hong Kong dollar bonds cannot be seen as a China proxy. “If you look at the issuers in the Hong Kong dollar space, except for the Chinese banks, most of them are Hong Kong issuers,” says Chandgothia.

Ang says that it has always been a struggle to find good Hong Kong dollar credit especially when doing a relative value against a US dollar credit. “But once in a while, especially during stressed times and when you see investors being forced to sell bonds, then we can get some at decent spreads.”

Both investors say that from a yield perspective it can be difficult to find value. “We regularly see the same credit pricing 20 to 30bp inside the dollar market,” Ang points out. “The whole question is whether Hong Kong dollar bonds can offer the same yield as in the US dollar fixed income market,” Chandgothia relates. “The answer is its lower than in the US dollar market. You look at 10-year treasuries; they are at about 150 to 155bp. Hong Kong is at about 1%.”

Comparing the return (carry and roll down) to the CNH market, Hong Kong dollar bonds is comparable. “A lot of the CNH yield comes from the currency yield,” Ang says. “On a theoretical asset-swap basis, the yield is actually not that great [for CNH].”

Still, Chandgothia believes the CNH market has one important advantage. “Ultimately, what’s going to happen is investors who have had the experience in dealing in CNH would have had some more exposure to Chinese issuers. When the onshore market opens up, they will be in the position to exploit that opportunity and that’s going to be a big opportunity.”

Additional reporting by Jacky Fung