Countries, including Malaysia, whose economies have higher levels of environment, social and governance (ESG) adoption have generally been safer and better shielded from the disruptions caused by the Covid-19 pandemic. At the same time, Islamic finance has demonstrated its resiliency in this difficult time with continuing issuances of green and sustainable sukuk – a trend that will continue over the short-to-medium term.

To this end, Malaysia’s Employees Provident Fund (EPF) – which manages the compulsory saving plan and retirement planning for the country’s private sector workforce and has assets under management (AUM) of 924.75 billion ringgit at the end of 2019 – is enhancing its focus on integrating different ESG initiatives into its investment strategy.

“With the pandemic, the key question at this time is how do we create a sustainable economy that is resilient enough to external shocks,” EPF chief investment officer Rohaya Mohammad Yusof told a webinar on Malaysia presented by The Asset Events+. “Countries with high [United Nations’] Social Development Goals (SDGs) index scores tend to fare better during the crisis.”

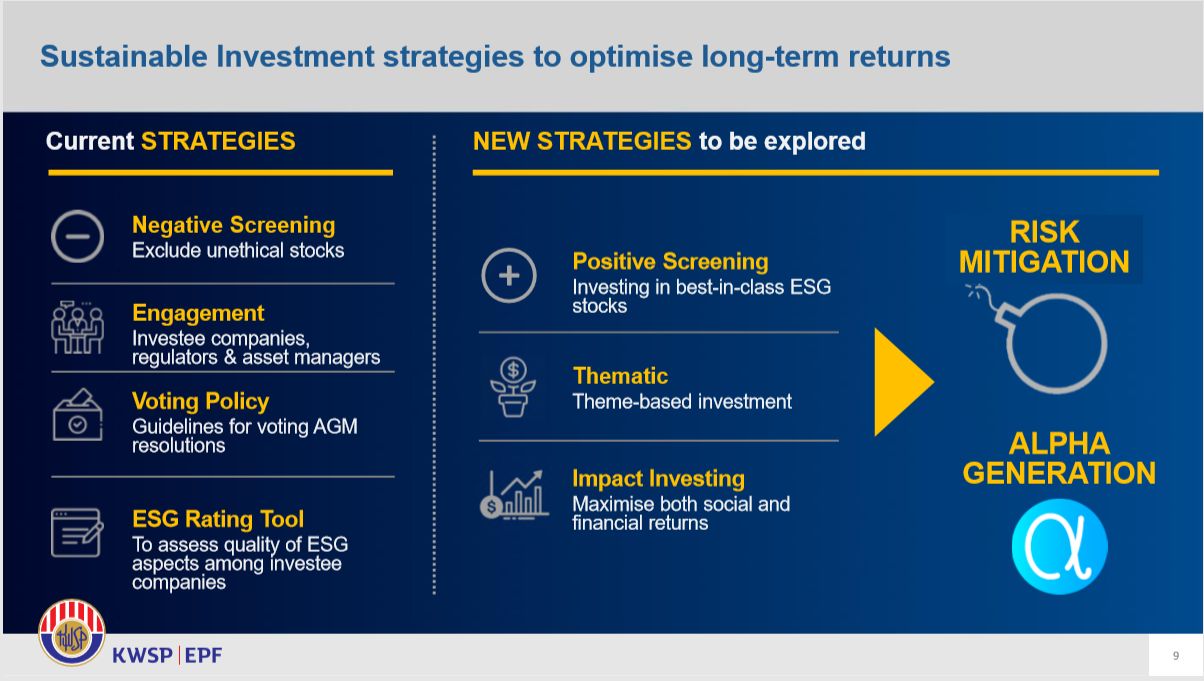

As part of the focus, the EPF will continue to explore new investment strategies that include screening for what Yusof describes as best-in-class ESG stocks. “We would like to invest in thematic stocks, such as those in renewable energy,” she notes. “What we see in this sustainable investment strategy is actually a risk mitigation scheme. At the same time, it provides an alpha generation.”

Illustrating the EPF’s current sustainable investment strategy, Yusof says the fund conducts negative screening and excludes those stocks that it considers unethical. It engages very closely with the investee companies, regulators and asset managers, and has a rating tool to assess the quality of ESG adoption at investee companies. The EPF also has its own internal voting policy, giving guidance on how the executives and directors vote on resolutions during annual general meetings.

The EPF did its own internal ESG assessment of the 10 top and bottom ESG stock performers. “What we saw is that in the mid-to-long term, they outperformed the Kuala Lumpur Composite Index,” Yusof explains. “ESG does not compromise returns – it actually gives better returns.”

For its part, Fitch Ratings in early 2019 launched an integrated scoring system that shows how ESG factors impact individual credit rating decisions. Its ESG approach fills a market gap by publicly disclosing how an ESG issue directly affects a company’s current credit rating.

Bashar Al-Natoor, global head of Islamic finance at Fitch Ratings, points out there is a lot of talk about the potential of Islamic finance not only on capital loss sharing and on partnership, but also on the charitable side. For instance, how to use waqf, which is defined as an Islamic endowment of property to be held in trust and used for charitable purposes, and how the Islamic finance industry can share the burden and make it more social.

Al Natoor notes how the issuers are tapping into the sukuk market for funding. For example, the Republic of Indonesia in June priced a three-tranche offering amounting to US$2.5 billion that included a US$750 million green sukuk. Also, in June, the Islamic Development Bank printed a US$1.5 billion debut sustainability sukuk in response to Covid-19, representing the first-ever AAA-rated sustainability in the global capital markets.

Banks in Malaysia are also pushing various ESG initiatives. This comes as Bank Negara Malaysia, the central bank, is coming up with a taxonomy that defines a green loan and ensures that banks indicate whether certain loans are green and, if so, how green they are.

“Investment banks are looking at how much of the advisory and financing that they’ve raised can be tagged as green,” says Yeoh Teik Leng, head of the capital markets group at AmInvestment Bank. “There is a focus on green types of assets, with a lot of banks looking to finance solar and hydro power projects. These initiatives by banks are independent of what the regulators are saying as we want to profile ourselves as being ESG champions.”

In 2018, AmInvestment Bank arranged the first ringgit-rated bonds issued under the Asean green bond standard amounting to 415 million ringgit to refinance the Gateway@klia2 Mall complex.

Affin Hwang Investment Bank’s push towards ESG is driven by its commitment to socially responsible investing (SRI). The bank’s deputy group managing director Yip Kit Weng notes that late last year the Securities Commission Malaysia announced a SRI roadmap and that fixed-income investors want more SRI and ESG-related investments. “As a bank, we are trying to match the supply and demand expectations for SRI and ESG-related paper,” he says.

Green and Islamic

In 2017, Affin Hwang Bank arranged the world’s first SRI sukuk for Tadau Energy to fund the construction of a solar farm project in Sabah. It arranged another SRI sukuk in 2018 for a solar project for Universiti Teknologi MARA – the first green financing undertaken by a public institute of higher education in Malaysia.

Malaysia’s national mortgage corporation, Cagamas Berhad, is targeting to launch its first sustainability bond or sukuk this year. It has already incorporated its sustainability framework into its conventional and Islamic medium-term note programmes.

“We are now able to issue sustainable bond/sukuk or SRI sukuk under this framework,” says Datuk Chung Chee Leong, Cagamas president and CEO. “We can incorporate different asset classes, including renewable energy, affordable housing, energy-efficient projects, green housing loans and green mortgages. All of these will help in our journey to meet our ESG objectives and also assist our investors to achieve their UN SDGs.”

Chung states that Cagamas will look at the benefits of social bonds and would like to emulate the pioneering actions of the Korea Housing Finance Corporation in this area.

Islamic bonds

When asked whether he noticed any liquidity stress among the Islamic banks in Islamic finance’s core market, Fitch's Al-Natoor notes that the pandemic's impact on oil prices has taken a toll on government funding in oil-exporting countries, including Malaysia and Gulf Co-operation Council (GCC) countries. This is crucial, he says, since this trickles down to the financial system. “If the oil prices are under pressure that means that bank liquidity is under pressure as well,” he points out. “This is important because it leads the financial institutions to being more selective in terms of lending.”

This situation, though, can be a catalyst for issuance activity for bonds and sukuk coming not just from the sovereigns, but also from the financial institutions and corporates. “This is positive in the short-to-medium term in the issuance volume as fund raising and diversification of funding become important,” Al Natoor adds.

Pandemic liquidity

Amid the Covid-19 pandemic in Malaysia, deal-making continued and the market remained flush with liquidity even during the lockdown in April. Affin Hwang’s Yip notes that banks and issuers/borrowers continued to exchange ideas on fund raising and corporate advisory. In fact, Affin Hwang and AmInvestment managed to complete tightly-priced transactions after generating sufficient demand.

“We’ve done some placements, and there is still some pent-up demand from investors for IPOs, which are coming back to the market. The IPOs, however, are rather small, compared with previous years. Clients are also discussing with us about refinancing or rescheduling their debt over the moratorium period,” Yip says.

AmInvestment’s Yeoh adds: “We make sure that our clients were taken care of. We approached certain clients to see whether they want to take advantage of the falling rates and tap the market to take advantage of the very flat yield curve.”

Cagamas remained open even during Malaysia’s movement control order and, in fact, it was able to issue 1.8 billion ringgit worth of bonds and sukuk during the first four weeks of the lockdown. “We needed to maintain operations as banks continued to talk to us about selling their assets, especially the housing loans,” Chung says. “It was important for Cagamas to continue to operate considering our role as a secondary liquidity provider to the financial system.”

The EPF’s Yusof agrees with Chung on the importance of liquidity during this challenging time. The EPF, she shares, ensures that its assets are liquid by putting them into tradeable instruments, whether its fixed income or equity. “This gives us a lot of freedom to manage our liquidity,” she points out. “Since we are managing multiple asset classes, this provides us with a lot of advantages to move from one class to another. But while fixed income has always been a hedging tool for us, this asset class has also demonstrated the same volatility as the equity during this crisis.”

For more information about the virtual event hosted by The Asset Events+ please go here.